Africa’s

electricity sector presents large investment opportunities for Independent

Power Producers

The

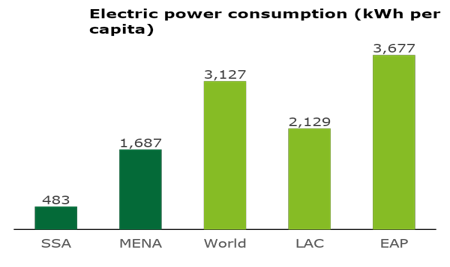

current level of access to electricity is remarkably low

Energy consumption in SSA is 3.5x lower than in MENA (exc. High-income countries) and 6.5x lower than the world average.

640 million people lack access to electricity on the continent.

Electricity blackouts occur on a daily basis in many African countries.

Africa faces a unique opportunity as nearly two-thirds of the additional capacity needed in 2030 is yet to be built.

Urbanization

and economic growth are driving demand for power

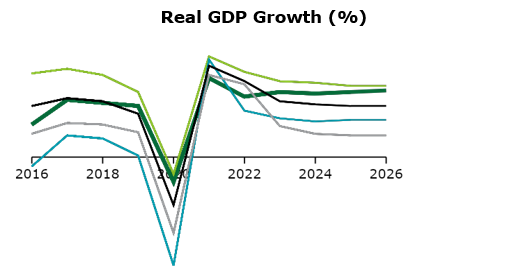

Many African countries such as Ivory Coast, Kenya, Ethiopia and Tanzania have sustained growth rates mostly above 5% p.a. before the covid-19.

The IMF forecasts an average growth rate of 4.3% p.a. in Africa over the 2021-2026 period.

Increased economic activity, fast urbanization, emerging industrial and mining sectors and a growing middle class are driving demand for power.

Significant generation capacity is expected to be added in the next decade

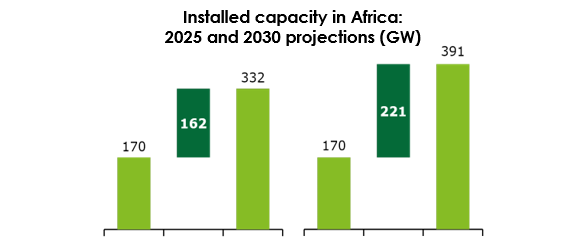

The AfDB is promoting an ambitious goal of achieving universal access to electricity by 2025 by adding 160 GW of on-grid generation.

IRENA estimates that Africa’s installed capacity in 2030 will range between 390 and 620 GW

With IPPs already representing a significant share of capacity (~25% in SSA, mostly in fossil-fuel plants), the development of Africa’s power sector will bring sizable investment opportunities for private developers.

The african power market

Renewables,

wind in particular, will capture an important share of additional generation

capacity in Africa

Renewables

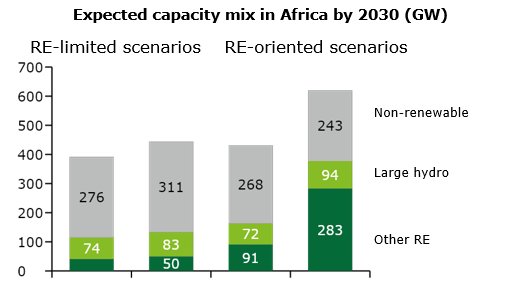

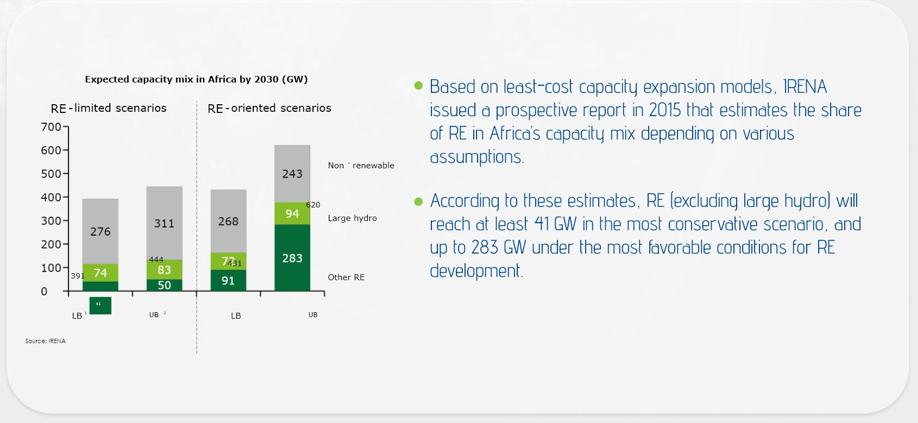

are expected to represent 30% to 60% of installed capacity by 2030

Based on least-cost capacity expansion models, IRENA issued a prospective report in 2015 that estimates the share of RE in Africa’s capacity mix depending on various assumptions.

According to these estimates, RE (excluding large hydro) will reach at least 41 GW in the most conservative scenario, and up to 283 GW under the most favorable conditions for RE development.

The

continuing decline in renewable costs is making them even more competitive

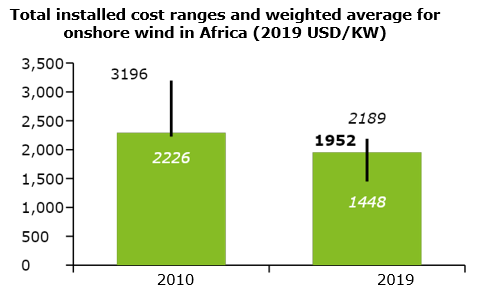

The total installed costs for wind projects in Africa declined by 14.8% between 2010 and 2019.

The Levelized Cost of Energy “LCOE” declined by 33% over the same period, reaching an average of USD 6.7cents, with some projects falling to USD 5 cents.

This trend is bound to continue based on recent auction prices and is making onshore wind more competitive than fossil-fuel alternatives in many African countries.

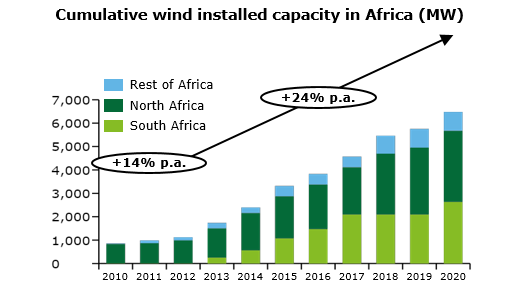

Installed wind capacity in Africa has started taking off

Installed wind capacity in Africa has increased ten-fold in the last decade, mainly driven by South Africa and North Africa, which added over 2,000 MW each.

Installed wind capacity for Africa, with the exception of South Africa, grew at an average of 16% p.a.. In 2020, the installed wind capacity for North Africa and Rest of Africa reached 3,844MW.

This growth is bound to accelerate as prices reach the tipping point where wind becomes cheaper than fossil-fuel alternatives in many countries.

CORPORATE STRATEGY

Focus on Gaia Energy Platform Africa « GEPA » Strategy

GEPA has a value-driven project development strategy

Early mover advantage and long-term value creation

Flexible pipeline allocation

Early mover in high growth countries with untapped resources gives GEPA a competitive advantage in terms of site selection, PPA negotiation, and discussions with the authorities

Focus on generating value throughout the lifecycle of the projects from early stage to financial close and COD

INVESTOR

Gaia Energy offers a compelling opportunity to invest in Africa’s promising renewable energy market

The market potential for wind in Africa is substantial

Africa’s wind power sector is at a crossroads. A number of markets on the continent are opening up to private investment at a time where wind technology is enabling more efficient generation at a lower cost.

This region is among the next target markets for wind given the untapped potential. Only 6.5 GW of current installed capacities, vs a potential wind capacity of 20-40 GW by 2030 if current trends continue according to management estimates.

Right time to enter the market in partnership with a true African developer with early mover advantage in a number of key markets.

Gaia Energy’s disciplined project screening allows the company to target all types of market segments:

Bilateral negotiations with Governments and local authorities, with the support of the Moroccan diplomacy.

Corporate PPA with industrials and private off-takers.

Tenders launched by local utilities.

GEPA

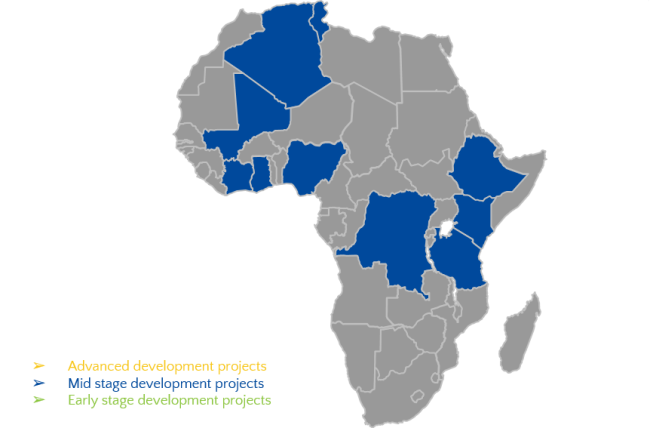

GEPA PIPELINE

Advanced development projects

Mid stage development projects

Early stage development projects

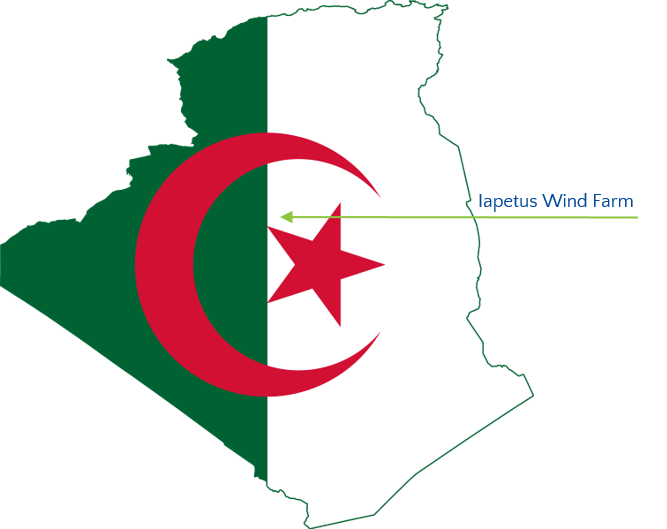

Iapetus Wind Farm

Technology : Wind

Capacity : 1 000 MW

CO2 emissions avoided : 3 400 000 Ton/Year

COD : -

Capex : 1 100 M€

Development stage : Early

Ratio of Country’s RE Capacity : 138%

Gaia Energy ALGERIA

lapetus

lapetus 1000MW

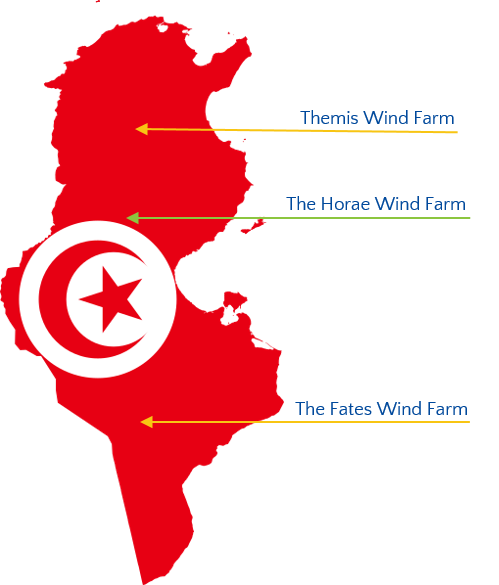

Themis Wind Farm

Technology : Wind

Capacity : 80 MW

CO2 emissions avoided : 272 000 Ton/Year

COD : -

Capex : 75 M€

Development stage : Advanced

Ratio of Country’s RE Capacity : 19%

Gaia Energy Tunisia

Themis

lapetus 1000MW

lapetus 1000MW

lapetus 1000MW

Themis Wind Farm

Technology : Wind

Capacity : 75 MW

CO2 emissions avoided : 255 000 Ton/Year

COD : -

Capex : -

Development stage : Mid

Ratio of Country’s RE Capacity : 4%

Gaia Energy GHANA

Theia , Eos

lapetus 1000MW

lapetus 1000MW

lapetus 1000MW

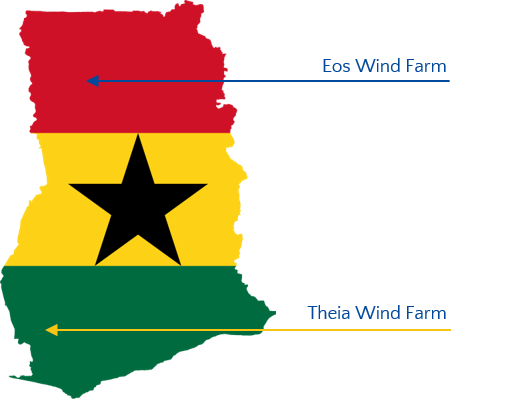

Themis Wind Farm

Technology : Wind

Capacity : 160 MW

CO2 emissions avoided : 544 000 Ton/Year

COD : 2026

Capex : 250 M€

Development stage : Early

Ratio of Country’s RE Capacity : 18%

Gaia Energy COTE D’IVOIRE

Coeus ,Leto

lapetus 1000MW

lapetus 1000MW

lapetus 1000MW

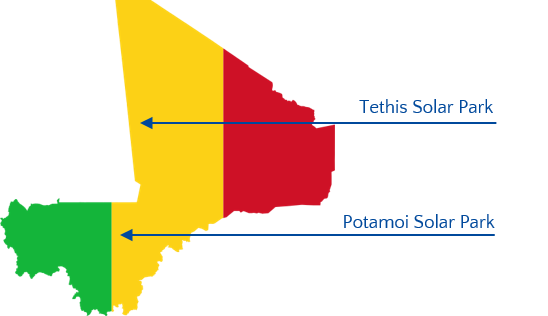

Tethis Solar Park 1

Technology : Solar

Capacity : 30 MWp

CO2 emissions avoided : 102 000 Ton/Year

COD : 2024

Capex : 20M€

Development stage : Mid

Ratio of Country’s RE Capacity : 8%

Gaia Energy MALI

Potamoi ,Tethis

lapetus 1000MW

lapetus 1000MW

lapetus 1000MW

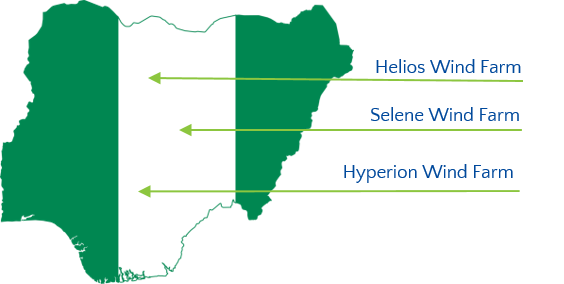

Helios Wind Farm

Technology : Wind

Capacity : 200 MW

CO2 emissions avoided : 680 000 Ton/Year

COD : -

Capex : -

Development stage : Early

Ratio of Country’s RE Capacity : 9%

Gaia Energy NIGERIA

Hyperion ,Selene ,Helios

lapetus 1000MW

lapetus 1000MW

lapetus 1000MW

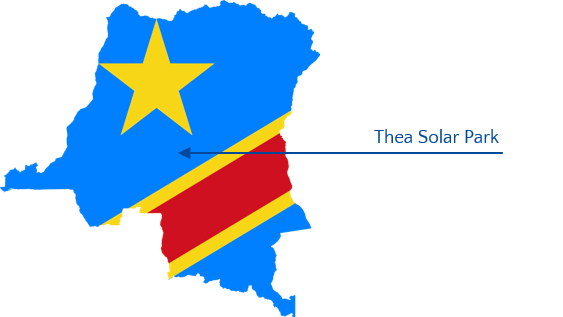

Thea Solar Park

Technology : Solar

Capacity : 250 MW

CO2 emissions avoided : 850 000 Ton/Year

COD : 2024/2025

Capex : 280 M€

Development stage : Mid

Ratio of Country’s RE Capacity : 100%

Gaia Energy CONGO DR

Thea

lapetus 1000MW

lapetus 1000MW

lapetus 1000MW

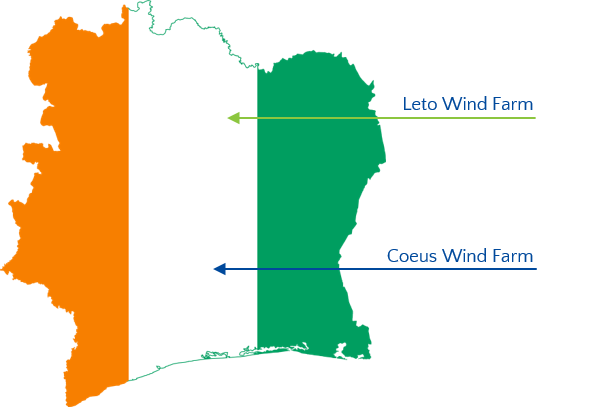

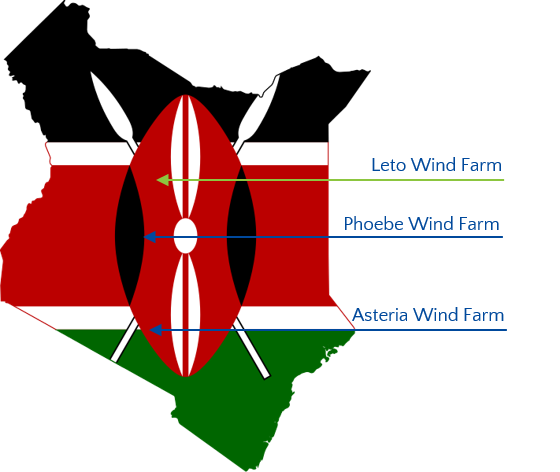

Leto Wind Farm

Technology : Wind

Capacity : 100 MW

CO2 emissions avoided : 340 000 Ton/Year COD : 2026

Capex : 150 M€

Development stage : Early

Ratio of Country’s RE Capacity : 4%

Gaia Energy KENYA

Asteria ,Phoebe ,Leto

lapetus 1000MW

lapetus 1000MW

lapetus 1000MW

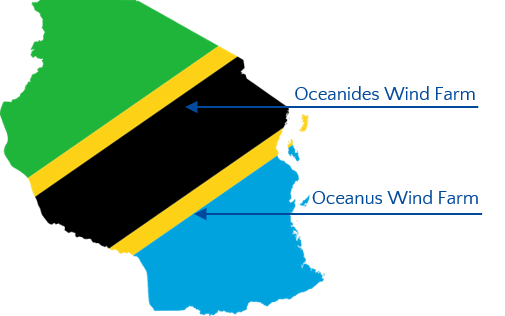

Oceanides Wind Farm

Technology : Wind

Capacity : 180 MW

CO2 emissions avoided : 612 000 Ton/Year

COD : -

Capex : 260 M€

Development stage : Mid

Ratio of Country’s RE Capacity : 27%

Gaia Energy TANZANIA

Oceanus ,Oceanides

lapetus 1000MW

lapetus 1000MW

lapetus 1000MW

our group

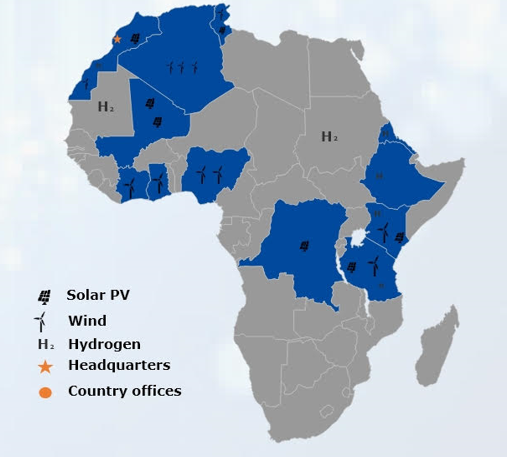

Gaia Energy, a pioneering RE-developer in Africa present in 12 countries

Gaia Energy, a pioneering RE-developer in Africa present in 12 countries

Gaia Energy has a geographically diversified pipeline and a strong local footprint with projects in 9 countries

Gaia Energy positions itself as a wind power developer with a long-term vision to become a leading African Independent Power Producer (“IPP”) with a diversified portfolio of large-scale RE projects.

The company has a distinctive approach to project development in Africa. It sources and develops multiple projects in parallel across carefully selected countries, with a proactive resource allocation to prioritize projects with a high likelihood of achieving Financial Close (“FC”) in the medium term.

Gaia Energy’s main objective is to deliver multiple RE projects cost effectively by creating economies of scale through local presence and synergies.

Gaia Energy focuses on wind power development, which requires a higher level of expertise with higher barriers to entry.

Gaia Energy’s African arm, GEPA, has capabilities to develop projects in Africa, recognized by leading players creating co-investment opportunities

Leveraging its local footprint and the support of a team of 30 people, Gaia Energy has a strong capacity to identify and originate attractive development or acquisition opportunities in countries with strong need of electricity.

The platform also benefits from the active support of Moroccan diplomacy to engage with government authorities throughout the continent in a constructive South-South cooperation approach.

Gaia Energy is committed to delivering high-quality bankable projects by working with the leading turbine manufacturers, and seeking support from renowned international tax, legal, technical and financial advisors.

gaia energy présentation

Gaia Energy provides RE development, reliable investments and specific services covering the whole life cycle of a project in wind and solar PV power plant up to financial close

Gaia Energy : Key characteristics

Founded in 2009, Gaia Energy is a pioneering independent large scale renewable energy developer in Africa.

Gaia Energy develops, owns and invests in RE projects, focusing mainly on wind and solar in high-growth African markets.

The company is leveraging on its local footprint, connection with the local decision makers and long experience, to identify and originate attractive development or acquisition opportunities in countries with strong need of electricity

The company has a distinctive approach to project development in Africa, with a proactive resource allocation to prioritize projects with a high likelihood of achieving Financial Close (“FC”) in the medium term.

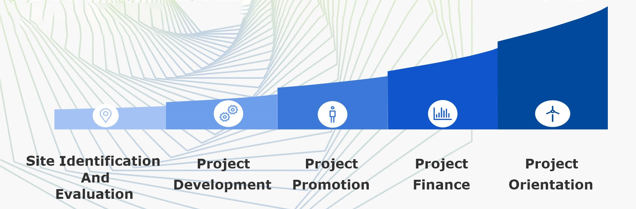

Gaia Energy has a long-term vision covering key stages of project development from origination to financial close

It combines technical, economical, fundraising and political expertise to local market, allowing to optimize the feasibility of the project.